I was in Washington, D.C., last week for a meeting, and one of the conversations at the table had to do with geopolitical risk in the context of doing business overseas. The discussion brought to light many concerns that U.S. firms have when examining the potential opportunity of new markets, especially those deemed as “emerging” by economic standards.

I was searching for some rank or measure to use – independent of financial analysis – to evaluate the stability of a country. I think I may have found such a measure.

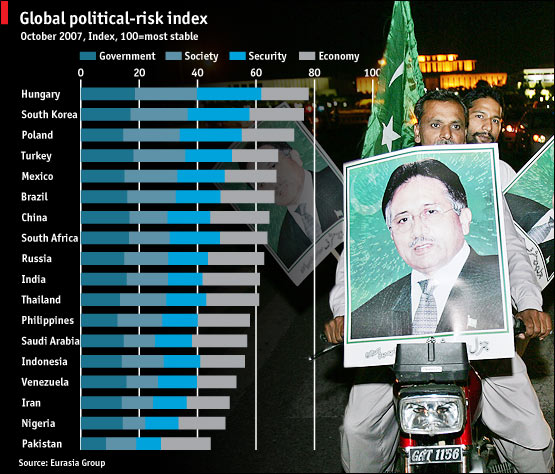

According to an article by The Economist, “Pakistan is rated as the least stable of 24 emerging markets surveyed in the Global Political Risk Index produced by Eurasia Group, a global political-risk consultancy. The monthly index uses a range of qualitative and quantitative indicators to measure both the capacity of countries to withstand shocks and their susceptibility to internal crises. Uncertainty over Pakistan’s political future, the country goes to the polls on October 6th, keeps it at the bottom. Iran and Nigeria vie with it for vulnerability to surprises. Hungary is considered the most likely to withstand trouble at home or from abroad.”

What’s interesting here is that South Korea, for example, is high on the list of risky places, but also ranks very high (32 out of 141) with regard to economic freedom.

The question then becomes, is it more advantageous to open your economy to new investments and development and hope such developments reduce risk, or is it better to stay closed and control the risk without the pressures of the broad market? And, as a firm, which risk is more easily mitigated — Those of the future of a country’s economy, or the future of its political structure? I clearly have more thinking to do on this topic and welcome any comments.